Filter by Categories or Explore All Articles Below.

Brian Giacomello I March 28, 2025

Brian Giacomello I March 4, 2025

March 3, 2025

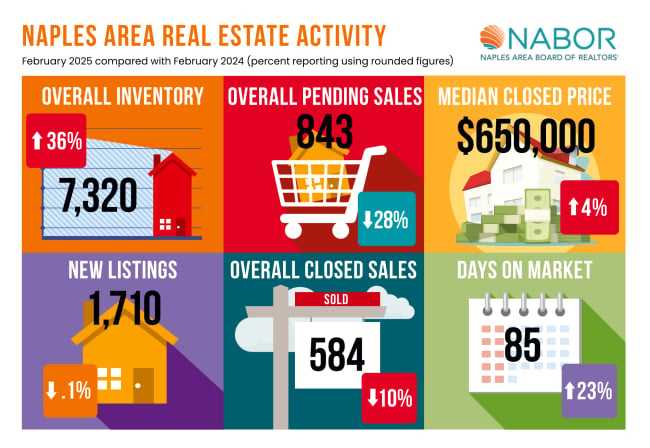

Brian Giacomello I February 27, 2025

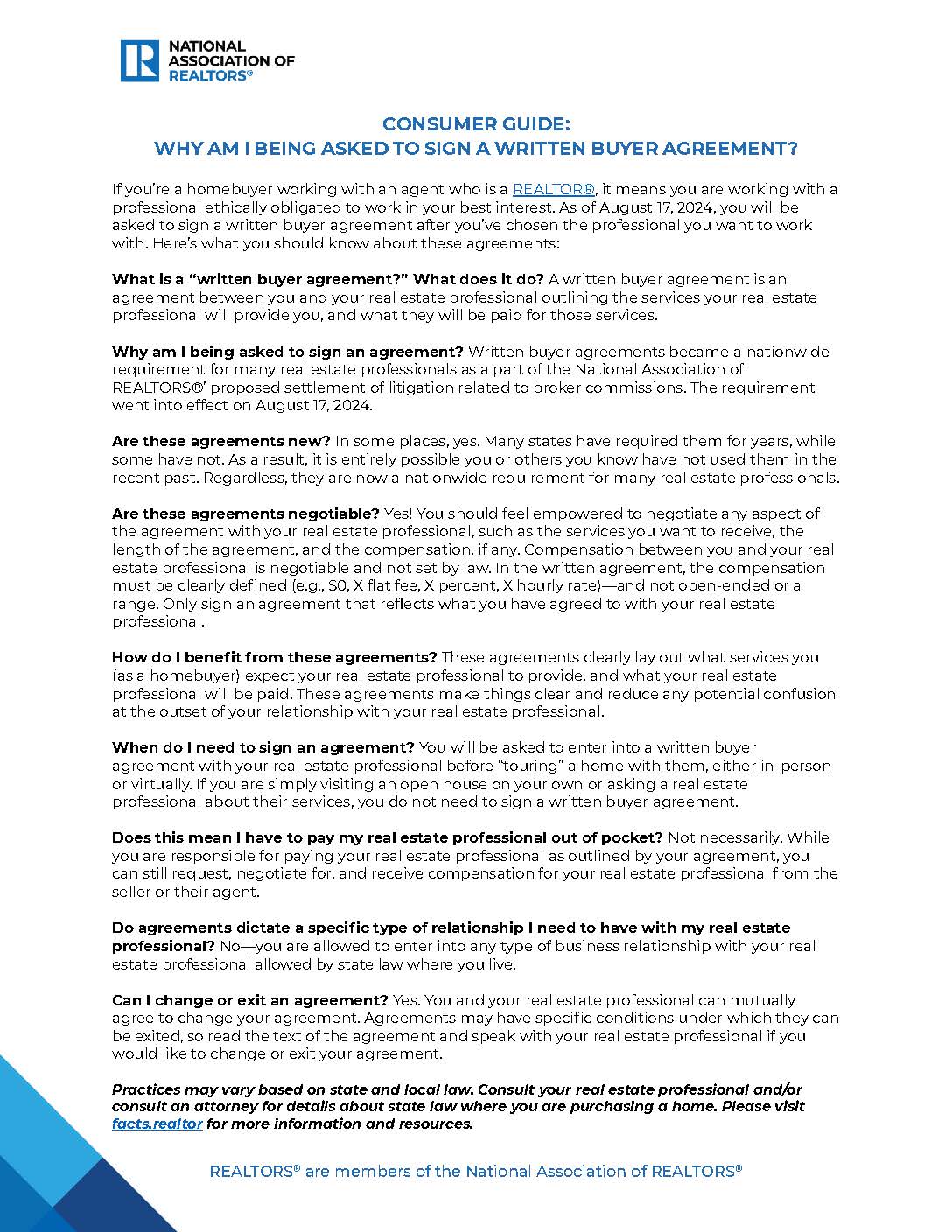

February 21, 2025

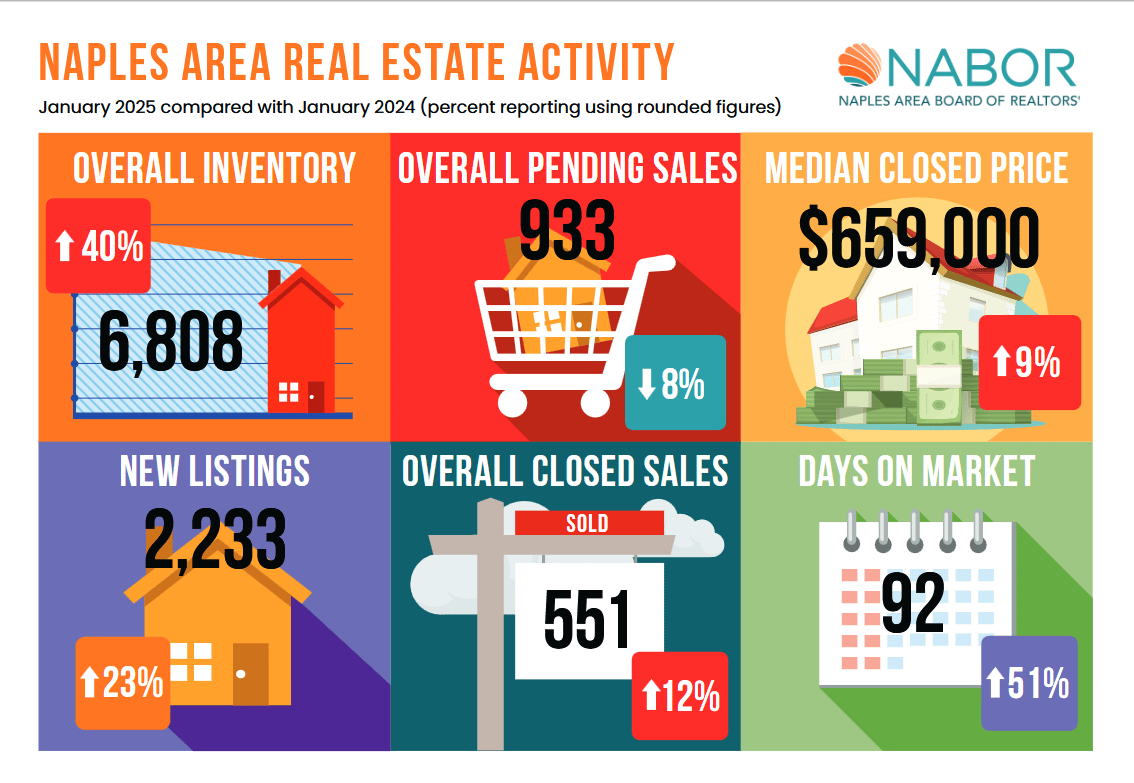

February 21, 2025

720 5th Ave S Naples FL 34102

720 5th Ave S Naples FL 34102